I can’t help but notice some folks talking on our social media about eye-popping price increases. I’m hearing talk of premiums doubling, or even tripling, since last year. What’s the story with this?

First of all, let’s set the record straight: if you were allowed to continue into 2016 the policy you bought in 2015, your rate may have gone up as much as 15-20% on www.healthcare.gov. That is a real price increase, on a real, apples-to-apples comparison of health insurance policies. It’s driven by the fact that our individual policies are currently losing large amounts of money. That’s because the premiums these customers are paying are far less than their medical costs, so we have to increase the premiums coming in to catch up and move us toward matching the actual cost of providing their healthcare. Those increases are real and valid.

In addition, federal regulations on how we must price health insurance include fixed age-price based ratios. This means that when we build products to sell, we have to use the rate a 21-year-old would pay as a baseline and rates increase between 1 and 3% each year simply because the insured got a year older. That is on top of the medical costs and baked into every health insurance policy sold in the individual market from coast to coast.

From the consumer perspective, unfortunately, we’ve seen some premiums skyrocket for other reasons that we here at Blue Cross cannot predict or control. Some are regulatory in nature, some are driven by the IRS and some are because we’ve had to discontinue certain products the federal government won’t let us sell anymore.

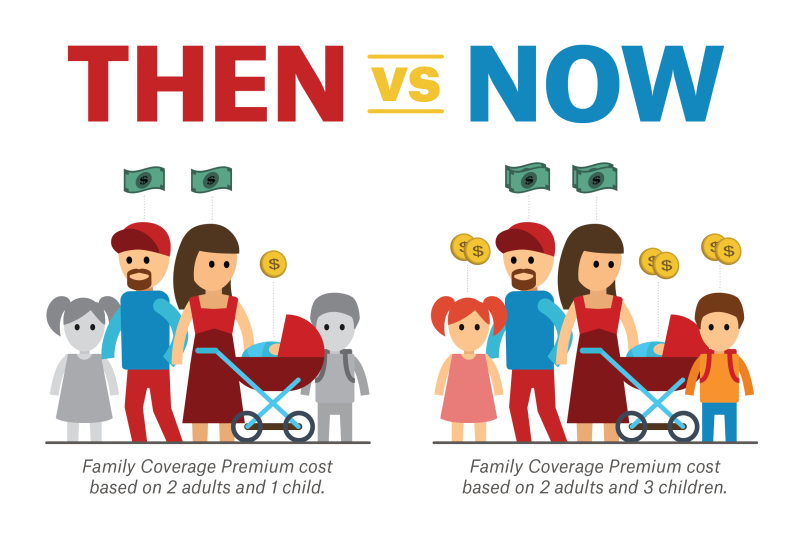

If you are buying coverage for several people in your household, say two adults and three children, your rates may have gone up because of a change in the definition of “family.” Just a few years ago, we bundled individual premiums into a “family” rate once three people were included in a plan. No matter how many children were added after the “family” threshold was reached, the rate did not go up. So three premiums (two adults and one child, for example) was the maximum any household had to pay.

New Federal exchange regulations have changed that.

Under the Affordable Care Act, new age-rating requirements shifted the cost of insurance away from those aged 50-64 and drove those costs onto child policies. Then, they required us to charge every child the new elevated premium in a household up to three children, not the single child required for “family” rates in the past.

This means larger families buying individual coverage are paying a lot more thanks to healthcare reform rules. Many of the huge rate increases we are seeing this month resulted from folks losing their “like-it, keep-it” plans that peaked at three member premiums. Those plans are now being converted to charge a premium for each adult family member, plus up to three children at the new, higher rates. So instead of three premiums total, a family of two adults and three children now pays five premiums with elevated child premiums. That’s a directive from Washington, D.C., that we cannot get around.

Other reasons for very large increases are not always so obvious. For example, when people buy insurance on www.healthcare.gov and receive federal assistance in the form of Advanced Tax Credits or Cost Sharing Reductions, this can mask the premium prices they are actually paying for insurance. So a 30-year-old with an income around $15,000 a year (as a single person) can get an insurance policy with a $390 actual premium each month by paying only $19/month. If this plan turns out to be his second-cheapest silver option, the plan will also have a deductible of $0. Once purchased, these rates may apply for an entire calendar year. That is high-quality insurance!

But each year he has this plan, www.healthcare.gov will re-evaluate his income based on his last tax return. And premium adjustments, sometimes substantial ones, can result if his income changes.

For example, if his income rises from $15,000 a year to $21,000 a year, his share of the premium will jump to $121 a month, a 636% increase! Did his insurance really go up that much? Of course not!

His actual premium might increase from $390 to $452 (a 16% increase) based on his age increasing and the medical expenses of other insured people, but www.healthcare.gov adjusted his federal assistance downward significantly because his income went up. This “reclassification” of income happens every year and sometimes DURING the year. In fact, “after-the-fact” audits of income led to more than 15,000 individuals losing their Blue Cross insurance during 2015, something we fought hard to avoid.

Unfortunately, once www.healthcare.gov turned off their advanced tax credits, some people were exposed to the full cost of their policy premiums, which was unaffordable for them. From the consumer perspective, all they know is their rates went from $20 a month to $452 a month, which they clearly cannot afford. As you can see from the explanation above, very little of this increase was insurance-company related. It was about the removal of the federal help they counted on to afford their premiums. These income-related adjustments happen all the time, and they can be confusing.

Another reason we sometimes see large rate changes is because of product changes required by the new federal definition of health insurance, sometimes called the Qualified Health Plan.

Prior to the passage of the Affordable Care Act, Blue Cross very successfully sold products that allowed the average buyer to decide how much of her medical risk she wanted to insure. For example, you could buy an insurance policy that covered you 100% if you were hospitalized, but outside the hospital you paid your own bills. Or you could add a few doctor visits. Or you could turn on, and turn off, maternity coverage as needed. Or you could cover some outpatient surgeries. Or not. The goal was maximum flexibility for the insured.

Insurance of that type gave the buyer complete control over the risk they assumed and people loved it, because it was flexible, and allowed them to buy as much coverage as they could afford at that stage of life. Typically, young folks bought this type of policy (or often their parents bought it for them) because younger folks are healthier, less prone to illness and have lower incomes, so these flexible policies fit their needs.

Until the Affordable Care Act passed, that is. Then the federal government declared flexibility a bad idea, the policies “junk” and ordered us to stop selling them and turn them off. We have been complying with that order for several months now, and this change affects tens of thousands of Louisianans whose choices are being rapidly reduced.

Any consumer moving from a “hospital-only” policy and being forced to buy the new, comprehensive policies sold in www.healthcare.gov, which cover EVERYTHING regardless of gender or medical need, is in for a shock when he sees the price differences. The new policies can easily cost double, triple, even four times as much because their coverage is so rich, and everyone is allowed to buy them (basically year round). Comparing the old plans to the new ones is not an apples-to-apples comparison but often the price increases are expressed that way. It’s like owning a Yugo, then being forced to buy a Ferrari and complaining about how much the price went up.

What can we do about this? Now that the federal government has stepped in and set the “basement” for health insurance so high, only they can undo that. So we continue to send data to the relevant federal agencies about the way things are going here.

I wrote this blog to help folks understand a few of these potentially expensive scenarios. It won’t lower your rates, but at least it might help spread the understanding of what is happening to the individual health insurance market under federal control.

So much for “if you like your plan you can keep it” and instead of saving $2500 per year per family on health insurance, premiums and deductibles went up to unaffordable levels for most consumers. I hope everyone who believed those promises, realizes they were taken Consumers should not have to pay for coverage they do not need. Fortunately, I did not believe any of it. The Unaffordable Health Care Act is unsustainable and hopefully will be replaced by something that is economically feasible, and is fair to the consumers who have been forced to purchase this awful product!

Wonderful article, wonderful author!

You are too kind! Blessings to you and your family!

mrb

Thanks for the guidance Mike – this blog will be very helpful to those who question the “sticker shock” of premium increases! As you mentioned, there are so many mandated variables that are drivers in the individual market, and, unless such are explained to policyholders in understandable verbiage (rather than Washington’s language), the individual market segment seems to think carriers are making the final premium decisions, wherein, Washington is the main driver. Thanks for shedding light to us all.

So my question is the “shared responsibility payments” or taxes as the Supreme Court calls them…..Are those payments/taxes returned to the insurance carriers as subsidies to defray the cost of providing care to your policyholders or are these taxes retained by the Federal Govt?

The “Individual Responsibility Requirement” and the “Employer Responsibility Requirement” payments in the ACA are fee/taxes just like any other, and go into the Federal General Fund and spent by Congress at their discretion. Insurance companies do not derive ANY benefit from these fees/taxes and in fact, there are several new fees and taxes from the ACA that we are required to raise locally and then SEND to Washington DC, like the insurer tax which cost our policyholders an additional $54m last year.

Thanks for the Question!….mrb