Do You Want Your Blue Cross Plan to Have Big Market Share?

Recently, I’ve read some news articles on a study talking about how concentrated health insurance markets are in different states. The study, thoughts from important officials and data all lead to one set of conclusions for our state:

Blue Cross and Blue Shield of Louisiana is too big. They need more competition in health insurance here in the state. Blue Cross has too much market share. It’s bad for the market. It’s bad for consumers.

Now, it’s the most natural thing in the world to be concerned about. Health insurance is expensive and critical to maintaining our health over the longer run, and we all believe competition is a healthy thing for prices.

Heck on its face, I find the argument rather compelling. More choices equals competitive prices, right?

“Blue Cross is just too big.” Let that roll around on your tongue for a while.

Ok, so now that I’ve set you up, here are a few things to consider.

Let’s just forget that actually, the biggest insurer in the state of Louisiana is the state itself, through the Medicaid program. Let’s also set aside the fact that more than 40 insurance companies have membership here in Louisiana besides Blue Cross. Let’s also set aside the fact that our real Louisiana market share is 1.1 million people out of the 4.65 million living in the state (which is about 24% of the market), and the fact that we are a not-for-profit company with federally regulated gross margins. With that aside, let’s ask some important questions:

How Big Do You Want Us to Be?

If you are a Blue Cross customer, do you want us to have a larger or smaller market share? Which is best for you, the consumer?

More than 85% of the money people paid us in premiums last year went right back out the door to pay their medical bills. We have contracts with pre-arranged payment amounts with thousands of doctors, around 100 hospitals and untold numbers of labs, imaging centers pharmacies and the like. We negotiate the rates with them, on your behalf, every single day, every single month, every single year. We are constantly pushing medical providers to make sure Blue Cross members are getting the best deal we can get for you.

Now, as a Blue Cross member, when I go to the bargaining table on your behalf, do you want me to be a smaller company? Or a company that brings more members and greater market share to the table? Which would you rather have?

Because remember, we represent you. We are paying your medical bills and are responsible for providing healthcare to you that you could never afford on your own. We are a not-for-profit, so it is impossible for us to make some far-off investors rich on your money; they don’t exist. We represent only you, our members, and it’s our job to make sure you get the right healthcare, in the right setting and at the right time, and that you get the absolute best deal when that happens. Size matters in those negotiations.

So Who Is Really Unhappy With Our Size?

I couldn’t help but notice that a lot of the research about market share of insurance companies and a lot of the press is generated by groups that represent… guess who? Yep, the guys on the other side of that negotiating table, doctors and hospitals.

The same guys from whom we are trying to get you the best deal are unhappy that they can’t make us smaller so they will have more leverage at bargaining time. I can’t blame them; if they can figure out a way to get bigger and take the leverage away from you, I’m sure they will do it. Fracturing the health insurance market works greatly in their favor. But our job is to make sure you get the best deal, not them.

Who Is Not Paying Their Share?

Don’t get me wrong, medical providers have been put in a very uncomfortable position. They are finding that more and more of their patients are insured by government programs, like Medicare and Medicaid. The government does not bargain with them at all. They give them a take-it-or-leave-it- price that is usually well below the cost these medical providers need to keep their lights on and doors open. A great example of this is Medicaid expansion in Louisiana.

In just the past 15 months, more than 400,000 Louisianans have signed up for the Medicaid expansion, bringing the total Louisiana population on Medicaid to 1.7 million. When these 1.7 million people go to the doctor or the hospital, the payments are so tiny compared to what healthcare actually costs that the providers go into the hole, big time, to make them well.

The same thing happens when the 550,000 Louisiana seniors on Medicare go to the doctor, but to a lesser effect since Medicare pays more (but still below cost). In just the past two years, the number of people insured by the government in Louisiana grew from 38% to more than 50%.More than half the people in the state are buying their healthcare below the docs’ and hospitals’ actual costs to provide it. A real, live loss that results from treating half the state’s market. How on earth can they make this up?

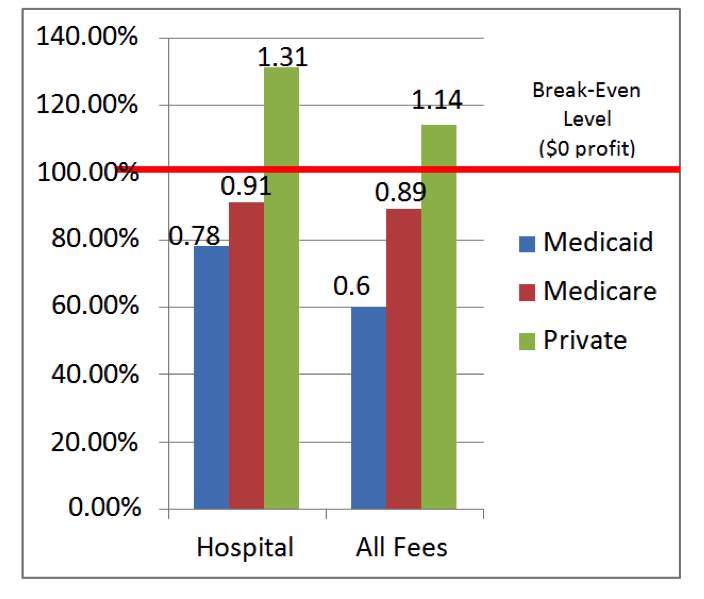

Yeah, you guessed it. They are looking for you, through your private insurance premiums to cover their losses. Take a look at this graphic to see what private insurance, Medicare and Medicaid pay compared to what providers need to break even. Just a few years ago, a national Blue Cross and Blue Shield Association study showed that up to 14% of your premiums are costs that have been shifted to you only because the government isn’t paying as much. But, they can’t get more money out of you — if we are big enough to stop them.

There Are No “Excess Profits”

Blue Cross is a not-for-profit company with federally specified gross margins. That’s a fancy way of saying you get rebates if we make too much money. That it is impossible for us to make “excess profits.” Even more interesting, your Blue Cross and Blue Shield of Louisiana consistently beats the federal requirement by spending less money than required on overhead and even more of your premium dollars directly on healthcare. In some years (like 2015), far more.

So, one thing that isn’t happening is that your hard-earned money and premiums are not being siphoned off to some nameless, faceless shareholders who live somewhere else. Your premiums are being spent here, buying healthcare for you. And last year, we ran our entire workforce in Louisiana on 6.8% of all the premiums you paid us. I challenge you to find any business out there that can run workforce and facilities costs at 6.8% of revenue. We run a VERY lean shop.

How lean? We operated eight regional offices, managed healthcare payments for 1.6 million people, paid doctors and hospitals more than $300 million a MONTH on behalf of our members and complied with all federal and state regulations and processed 31 million claims – all on 6.8% of your premiums. That’s what it cost us to manage our workforce and our business. We are very efficient.

I’d even go so far as to say that one reason there might not be more competitors in the marketplace who are as large as we are is because we are so efficient. And, you’d have to be better than us to take market share away from us.

Other companies come in and try to compete here. Frankly, I love it when that happens because it gives us a chance to sharpen our axes and get even better for you. But, they have failed in the past because we are frankly hard to compete against. We are efficient and work hard to get you the best prices on the healthcare you need. Remember, 85% of your premiums is simply the cost of healthcare we buy for you. (Taxes eat another 4%, and payments we make to brokers who work with your employers eat up another 4%.)

What does all that mean?

Our size and our market share give you an advantage when you are buying healthcare or health insurance. We know that the 85% of your money we are using to buy healthcare is going to face upward pricing pressure every year. Facing a future where more and more people are insured by government programs, medical providers are going to push harder and harder for you to make up that difference through your premiums. If we are smaller, we cannot effectively fight them off. Our size is our best defense at trying to put the brakes on a runaway train that is the cost of medicine. And our defense is your defense.

We represent you. So I’ll ask you again:

Do you want us to be smaller? Do you want us to have less market share? Do you want us to lose our leverage when we bargain on your behalf?

Isn’t it just possible that we are large because we are invested in Louisiana like no other health insurance company is, that we do a great job and that we belong to our members?

Straight Talk is no matter what our market share turns out to be, bigger is better for you.

{kind=link}

Leave a Reply