Who Allows These Companies to Make Such Massive Profits?

Blue Cross has an active social media presence on Facebook, Twitter and Pinterest. We got the Facebook message above from a member, and this is my response.

Frustration with the prices of health insurance is a common theme during this open enrollment period, which ends Jan. 31, 2016. We got the message above on Facebook recently, and as a Blue Cross member, the author is entitled, as are all our members entitled, to all the transparency our financial statements can give. In this post, I’m going to lay out our finances here at Blue Cross and Blue Shield of Louisiana for all of our members to see. It’s only fair. I can’t put any money back into the member’s pocket, but she surely deserves to know where her money went.

Let’s start with 2014, since I have complete financial data for that entire year.

On behalf of our fully insured group members and individual customers (like the ones who buy insurance on www.healthcare.gov) I can report that last year we took in $2.83 billion in premiums during 2014, right here in Louisiana.

Yes, almost $3 billion. This is a staggering sum by any measure. It is CRITICAL to me that our members/owners know where every single dollar went. Let’s start with the basics:

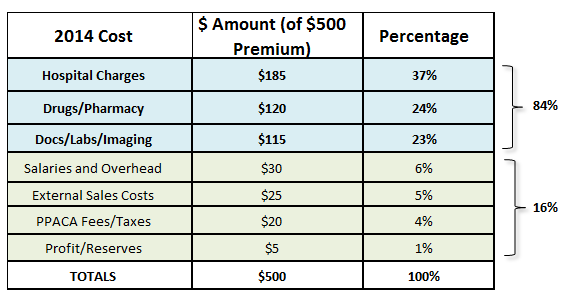

During 2014, we sent 37% of that sum, more than $1 billion, directly to the hospitals around the state and nation that cared for our members. So for every dollar you paid in premiums, 37 cents of it went straight to hospitals. Or to think of it another way, if your premium was $500/month, $185 of that money went straight to a hospital.

Likewise, we spent 24% of the money on prescription drugs for our members — about $679 million. Of our $500 premium, that’s another $120 that bought medications for our members.

Another 23% of the money, about $651 million, paid for doctor visits, lab tests, imaging and outpatient surgery-type expenses. That’s $115 of the premium. So far we’ve accounted for 84% of the premiums paid in, or roughly $420 of the $500 monthly premium. What about the rest of it, the other $80?

About $20 of our imaginary $500 premium, or 4% more, went directly to the government in the form of taxes and fees. And 6% of the total, around $30, paid the salaries of every Blue Cross employee and the overhead of running our operations. Another 5%, or $25, paid all the outside entities that help companies buy insurance and take care of the individual customers, many of whom bought insurance for the first time during 2014 on www.healthcare.gov.

When all the expenses were paid last year, we had about 1% (about $5 of the $500) left over. Since we are a not-for-profit company, that money went into a bank account for a rainy day. Here’s a table to sum up where that money went, based on the $500/month premium I mentioned above:

If you call what we had left over in 2015 “profit,” it was about 1% of the total collected. About $5 on the $500 premium. That was last year.

2015 will be different. The stress and strains of providing care for a new and burgeoning population of people with federally-specified insurance that requires people to carry a lot more coverage than what most of them had before will change our financials drastically in 2015.

That “Profits/Reserves” last line will have a large, negative number in it at the end of 2015, even as we shrink “external sales costs” and “salaries and overhead” by millions of dollars. And we will be living off of our savings to make ends meet in 2015 and into 2016 as well. Blue Cross will lose money this year. Luckily, we are a Louisiana-strong company with an 80-year history in this state, and we have reserves to keep us strong for a while. But, we need to think long-term and see how we can right the ship soon and consider other options.

And if you were wondering how the government fits into all this? There is a federal law that guarantees that we can’t make massive profits. The law says we have to run our entire operation, which is all of our operating costs other than the medical expenses, on no more than 15% of the money we take in (on our largest customers) or 20% of the money we take in (on individuals and small companies). No insurance company is allowed to operate on more than that; if they do, they have to pay rebates to their members/owners. (That’s you.) The first three lines in the table above should add up to at LEAST 80%, or your insurance company has to give you money back. You can see in 2014 our first three lines are 84%.

I know this explanation won’t lower your premiums any or put any more money in your pocket, but you deserve to know exactly what’s happening and why. There are no “massive profits” here at Blue Cross, and, if there were, we’d be THRILLED to lower rates and put a smile on our customer’s faces. Surrounded by our customers every day, more than 1 in 3 Louisianans, how could we not take pleasure in improving your financial situation? We live, work and do business right alongside them. You’re our neighbors, friends and family members.

Nothing would make me happier, I can tell you that.